Total asset turnover is computed as net sales /average total assets.

Bina Co. purchased a vehicle on January 1st, for $15,000 and estimates it will use the vehicle for

eight years with a $3,000 salvage value. Using the double declining-balance depreciation method,

compute the vehicle's second year depreciation expense.

$3,000.00

$2,812.50

$2,250.00

$3,750.00

Amortization expense is recorded on which financial statement?

Income statement

Balance sheet

Statement of retained earnings

__ is measured as the excess of the cost of an acquired entity over the value of the acquired net

assets.

Patent

Goodwill

Leasehold

Copyright

A company acquires a patent for $20,000 to manufacture and sell an item. The company intends to hold

the patent for 5 years. Amortization for the first year will be recorded with a debit to Amortization Expense

for $4000.

Wednesday, November 27, 2019

Keva Co. trades in a vehicle with an original cost of $20,000 and accumulated depreciation of $18,000

Keva Co. trades in a vehicle with an original cost of $20,000 and accumulated depreciation of

$18,000. The list price of the new vehicle is $25,000. In addition to the old vehicle, Keva also

provides $24,000 cash. The ent/y to record this transaction would include debits to which of the

following accounts? (Check all that apply.)

Vehicles for $25,000

Accumulated Depreciation-Vehicles for $18,000

Loss on Exchange of Vehicles for $1,000

Book value fs $20,000-$1.8,000=$1!,000. Asset received = $25,000

- assets gjven $2,000 book-value+ $24,000 = $2.6,000. Loss= $25 000 26 000 ~ $1,000.

Cash for $24,000

Gain on Exchange of Vehicles for $1,000

An oil company recognizes the cost of discovering and operating oil wells by recording __ _

expense for each unit of oil used.

operating

depletion

depreciation

amortization

Goodwill is the amount by which a company's value exceeds the value of its individual assets and

liabilities. It is recorded as an intangible asset, but is not amortized.

Which of the following items related to depreciating equipment would be found on a company's

income statement?

Depreciation Expense - Equipment

Accumulated Depreciation - Equipment

Equipment

Net Book Value

$18,000. The list price of the new vehicle is $25,000. In addition to the old vehicle, Keva also

provides $24,000 cash. The ent/y to record this transaction would include debits to which of the

following accounts? (Check all that apply.)

Vehicles for $25,000

Accumulated Depreciation-Vehicles for $18,000

Loss on Exchange of Vehicles for $1,000

Book value fs $20,000-$1.8,000=$1!,000. Asset received = $25,000

- assets gjven $2,000 book-value+ $24,000 = $2.6,000. Loss= $25 000 26 000 ~ $1,000.

Cash for $24,000

Gain on Exchange of Vehicles for $1,000

An oil company recognizes the cost of discovering and operating oil wells by recording __ _

expense for each unit of oil used.

operating

depletion

depreciation

amortization

Goodwill is the amount by which a company's value exceeds the value of its individual assets and

liabilities. It is recorded as an intangible asset, but is not amortized.

Which of the following items related to depreciating equipment would be found on a company's

income statement?

Depreciation Expense - Equipment

Accumulated Depreciation - Equipment

Equipment

Net Book Value

Diamond Co. paid cash to overhaul a forklift, which extended the life of the forklift for an additional four years.

To calculate depletion expense, first determine the depletion per unit. Depletion per unit can be

calculated by taking (cost total units of capacity.

+ operating expenses

operating expenses

salvage value

+salvage value

Diamond Co. paid cash to overhaul a forklift, which extended the life of the forklift for an additional

four years. The entry to record this purchase would include a debit to the ___ account.

Repairs & Maintenance Expense

Equipment

Depreciation Expense - Equipment

Cash

If an intangible asset has a limited life, its cost is systematically allocated to expense over its useful

life through the process of:

amortization

depreciation

depletion

impairment

_____ are expenditures that extend the assets useful life beyond its original estimate.

calculated by taking (cost total units of capacity.

+ operating expenses

operating expenses

salvage value

+salvage value

Diamond Co. paid cash to overhaul a forklift, which extended the life of the forklift for an additional

four years. The entry to record this purchase would include a debit to the ___ account.

Repairs & Maintenance Expense

Equipment

Depreciation Expense - Equipment

Cash

If an intangible asset has a limited life, its cost is systematically allocated to expense over its useful

life through the process of:

amortization

depreciation

depletion

impairment

_____ are expenditures that extend the assets useful life beyond its original estimate.

Revenue expenditures

Extraordinary repairs

Betterments

Ordinary repairs

___ are expenditures that keep an asset in normal, good operating condition. They are necessary

if an asset is to perform to expectations over its useful life.

Ordinary Repairs

Grand Co. trades in an old machine for a new machine. The new machine has a list price of $10,000. The old machine has a cost of $12,000

A patent was purchased for $20,000 and expected to be used for the 20-year life with no salvage

value. The entry to expense the patent during the· second year of life will include which of the

following entries? (Check all that apply.)

Credit to Accumulated Amortization $1,000.

Debit to Amortization Expense $1,000.

Debit to Accumulated Amortization $1,000.

Credit to Amortization Expense $1,000.

Zion Co. paid cash for an upgrade to an existing machine that would reduce the amount of waste

produced by the machine (and therefore, Increasing efficiency). The journal entry to record this

upgrade would Include which of the following entries? (Check all that apply.)

Debit to Machinery

Debit to Repair & Maintenance Expense

Credit to Repair & Maintenance Expense

Credit to Machinery

Credit to Cash

Debit to Cash

Grand Co. trades in an old machine for a new machine. The new machine has a list price of $10,000. The

old machine has a cost of $12,000 and accumulated depreciation of $9,000. In addition, Grand will pay

$6,000 towards the purchase. Because the new machine is much more technologically advanced, the

exchange has commercial substance. The trade will include a (gain/loss) gain of $1000.

value. The entry to expense the patent during the· second year of life will include which of the

following entries? (Check all that apply.)

Credit to Accumulated Amortization $1,000.

Debit to Amortization Expense $1,000.

Debit to Accumulated Amortization $1,000.

Credit to Amortization Expense $1,000.

Zion Co. paid cash for an upgrade to an existing machine that would reduce the amount of waste

produced by the machine (and therefore, Increasing efficiency). The journal entry to record this

upgrade would Include which of the following entries? (Check all that apply.)

Debit to Machinery

Debit to Repair & Maintenance Expense

Credit to Repair & Maintenance Expense

Credit to Machinery

Credit to Cash

Debit to Cash

Grand Co. trades in an old machine for a new machine. The new machine has a list price of $10,000. The

old machine has a cost of $12,000 and accumulated depreciation of $9,000. In addition, Grand will pay

$6,000 towards the purchase. Because the new machine is much more technologically advanced, the

exchange has commercial substance. The trade will include a (gain/loss) gain of $1000.

Seven Co. owns a coal mine with an estimated 1,000,000 tons of available coal. It was purchased for $300,000 and has $50,000 salvage value.

Trio Co. reported that maintenance and repair costs are expensed as incurred. If Trio's current year

machinery and equipment repair costs are $8,200, which accounts would be Impacted to complete

the journal entry? (Check all that apply.)

Credit Repairs expense.

Debit Repairs expense.

Credit Machinery & equipment

Debit Machinery & equipment

Credit Cash.

Debit Cash.

The process of allocating the cost of a natural resource to a period when it is consumed requires a debit

entry to the Depletion Expense account.

Seven Co. owns a coal mine with an estimated 1,000,000 tons of available coal. It was purchased for

$300,000 and has $50,000 salvage value. During the current period, Seven mined and sold

200,000 tons of coal. Depletion expense for the period will be how much?

machinery and equipment repair costs are $8,200, which accounts would be Impacted to complete

the journal entry? (Check all that apply.)

Credit Repairs expense.

Debit Repairs expense.

Credit Machinery & equipment

Debit Machinery & equipment

Credit Cash.

Debit Cash.

The process of allocating the cost of a natural resource to a period when it is consumed requires a debit

entry to the Depletion Expense account.

Seven Co. owns a coal mine with an estimated 1,000,000 tons of available coal. It was purchased for

$300,000 and has $50,000 salvage value. During the current period, Seven mined and sold

200,000 tons of coal. Depletion expense for the period will be how much?

$30,000

$60,000

$50,000

____ are expenditures that make a plant asset more efficient or productive, but do not always

increase an asset's useful life.

Revenue expenditures

Ordinary repairs

Extraordinary repairs

Betterments

Ion Co. purchased land for $190,000. Ion also paid $5,000 in brokerage fees, $1,000 in legal fees,

and $500 in title costs. Ion should record the cost of this land to be:

$196,500

$190,000

$195,500

$196,000

$195,000

At the beginning of the year, Jobs Co. owned one piece of office equipment, a copier. The copier was purchased two years ago for $12,000

Which of the following assets are amortized? (Check all that apply.)

Coal mine

Patent

Land

Building

Copyright

Geo Co. purchased a building for $400,000. In addition, Geo paid $35,000 closing fees (including

brokerage, title, and attorney fees). Geo also paid $60,000 to modify the building, changing the layout

specifically for Geo's needs. Geo should record the building at $495000.

$400,00035,00060,000=$495,000

Land improvements are assets that Increase the benefits of land, have a limited useful life, and are

depreciated-such as sidewalks and fences.

Book value can be calculated by taking an asset's acquisition costs less its accumulated depreciation.

At the beginning of the year, Jobs Co. owned one piece of office equipment, a copier. The copier was

purchased two years ago for $12,000. At the beginning of the year, the balance in accumulated

depreciation was $4,000. Jobs uses straight-line depreciation of $2,000 per year with a zero salvage

value. How much is accumulated depreciation at the end of the year?

$10,000

$2,000

$4,000

$6,000

$12,000

$8,000

Coal mine

Patent

Land

Building

Copyright

Geo Co. purchased a building for $400,000. In addition, Geo paid $35,000 closing fees (including

brokerage, title, and attorney fees). Geo also paid $60,000 to modify the building, changing the layout

specifically for Geo's needs. Geo should record the building at $495000.

$400,00035,00060,000=$495,000

Land improvements are assets that Increase the benefits of land, have a limited useful life, and are

depreciated-such as sidewalks and fences.

Book value can be calculated by taking an asset's acquisition costs less its accumulated depreciation.

At the beginning of the year, Jobs Co. owned one piece of office equipment, a copier. The copier was

purchased two years ago for $12,000. At the beginning of the year, the balance in accumulated

depreciation was $4,000. Jobs uses straight-line depreciation of $2,000 per year with a zero salvage

value. How much is accumulated depreciation at the end of the year?

$10,000

$2,000

$4,000

$6,000

$12,000

$8,000

On October 30, Cleo Co. purchased a machine for $26,000 and estimates it will use the machine for four-years wlth a $2,000 salvage value

(Capital/Revenue)Capital expenditures are additional costs of plant assets that provide benefits

extending beyond the current period, such as a plant expansion, or machine overhaul.

Consistent with the principle, plant assets should be recorded at cost, which includes all

the normal and reasonable expenditures necessary to get the asset in place and ready for its

intended use.

monetary unit

plant asset

cost

full disclosure

___ are nonphysical assets (used in operations) that confer on their owners long-term rights,

privileges, or competitive advantages.

Natural resource

Intangible assets

Plant assets

Current assets

Accumulated depreciation is a contra asset account (one that is linked with the plant asset account, but

has an opposite normal balance) and is reported on the balance sheet.

(Plant;Current)Plant assets purchased as a group in a single transaction for a lump-sum price (also called

a lump-sum, group, bulk, or basket purchase) are allocated the purchase price based on their relative

market values.

On October 30, Cleo Co. purchased a machine for $26,000 and estimates it will use the machine for

four-years wlth a $2,000 salvage value. Using the straight-line depreciation method, compute the

machine's first year partial depreciation expense for October 30 through December 31.

$6,000

$1,000

$1,500

$3,000

extending beyond the current period, such as a plant expansion, or machine overhaul.

Consistent with the principle, plant assets should be recorded at cost, which includes all

the normal and reasonable expenditures necessary to get the asset in place and ready for its

intended use.

monetary unit

plant asset

cost

full disclosure

___ are nonphysical assets (used in operations) that confer on their owners long-term rights,

privileges, or competitive advantages.

Natural resource

Intangible assets

Plant assets

Current assets

Accumulated depreciation is a contra asset account (one that is linked with the plant asset account, but

has an opposite normal balance) and is reported on the balance sheet.

(Plant;Current)Plant assets purchased as a group in a single transaction for a lump-sum price (also called

a lump-sum, group, bulk, or basket purchase) are allocated the purchase price based on their relative

market values.

On October 30, Cleo Co. purchased a machine for $26,000 and estimates it will use the machine for

four-years wlth a $2,000 salvage value. Using the straight-line depreciation method, compute the

machine's first year partial depreciation expense for October 30 through December 31.

$6,000

$1,000

$1,500

$3,000

On December 31, Briar Co. disposed of a piece of equipment that cost $6,000 with accumulated depreciation of $4,500.

Ironworks Co. sells a machine that cost $5,000 with a current book value of $1,500 for $2,000 cash.

Ironworks will record a debit to which account and for how much?

Accumulated Depreciation - Equipment for $:ll,500

Equipment for $5,000

Equipment for $3,500

Accumulated Depreciation - Equipment for $3,500

Prive Co. purchases a machine that cost $15,000. Prive estimates a 5-year life with no salvage value.

The first three years of depreciation expense are $6,000; $3,600; and $2,160, respectively. Based

on this information, Prive is using the ___ depreciation method.

straight-line

declining-balance

units-of-production

On December 31, Briar Co. disposed of a piece of equipment that cost $6,000 with accumulated

depreciation of $4,500. The entry to record this disposal would include a debit to which account and

for how much?

Depreciation Expense - Equipment for $1,500

Loss on Disposal of Equipment for $1,500

Accumulated Depreciation for $6,000

Equipment for $6,000

The method of depreciation that charges a varying amount to depreciation expense for each period of

an asset's useful life depending on Its usage is called the method.

straight-line

MACRS

units-of-production

declining-balance

Ironworks will record a debit to which account and for how much?

Accumulated Depreciation - Equipment for $:ll,500

Equipment for $5,000

Equipment for $3,500

Accumulated Depreciation - Equipment for $3,500

Prive Co. purchases a machine that cost $15,000. Prive estimates a 5-year life with no salvage value.

The first three years of depreciation expense are $6,000; $3,600; and $2,160, respectively. Based

on this information, Prive is using the ___ depreciation method.

straight-line

declining-balance

units-of-production

On December 31, Briar Co. disposed of a piece of equipment that cost $6,000 with accumulated

depreciation of $4,500. The entry to record this disposal would include a debit to which account and

for how much?

Depreciation Expense - Equipment for $1,500

Loss on Disposal of Equipment for $1,500

Accumulated Depreciation for $6,000

Equipment for $6,000

The method of depreciation that charges a varying amount to depreciation expense for each period of

an asset's useful life depending on Its usage is called the method.

straight-line

MACRS

units-of-production

declining-balance

A company sells a machine that cost $7,000 for $500 cash. The machine had $6,500 accumulated depreciation.

A company owns an asset that Is fully depreciated. The asset is no longer being used in operations

and has no market value. The company has decided to ___ the asset by recording an entry to

remove it from the balance sheet.

discard

depreciate

take a loss on

Straight-line depreciation is calculated by taking cost - (salvage/market)salvage value.

Depreciation is the process of allocating the cost of a plant asset to expense in the accounting periods

benefiting from its use.

Brice Co. purchases land in order to drill oil. This land would be classified as a{n) ___ on the

balance sheet.

and has no market value. The company has decided to ___ the asset by recording an entry to

remove it from the balance sheet.

discard

depreciate

take a loss on

Straight-line depreciation is calculated by taking cost - (salvage/market)salvage value.

Depreciation is the process of allocating the cost of a plant asset to expense in the accounting periods

benefiting from its use.

Brice Co. purchases land in order to drill oil. This land would be classified as a{n) ___ on the

balance sheet.

plant asset

intangible asset

current asset

natural resource

A company sells a machine that cost $7,000 for $500 cash. The machine had $6,500 accumulated

depreciation. The entry to record this transaction will Include which of the following entries? (Check

all that apply.)

On January 3, ATA Company purchases a copy machine for $11,500. The machine is expected to last five years and have a salvage value of $1,500

The factors necessary to compute depreciation include (cost selling price/market value)cost, salvage

value and useful life.

___ value, also called residual value or scrap value, is an estimate of the asset's value at the end

of its benefit period.

Leftover

Useful

Obsolescence

Salvage

On January 3, ATA Company purchases a copy machine for $11,500. The machine is expected to last

five years and have a salvage value of $1,500. Compute depreciation expense for the first year,

assuming the company uses the straight-line method.

$2,300

$2,000

$2,600

value and useful life.

___ value, also called residual value or scrap value, is an estimate of the asset's value at the end

of its benefit period.

Leftover

Useful

Obsolescence

Salvage

On January 3, ATA Company purchases a copy machine for $11,500. The machine is expected to last

five years and have a salvage value of $1,500. Compute depreciation expense for the first year,

assuming the company uses the straight-line method.

$2,300

$2,000

$2,600

The useful life (also called service life) is the length of time the asset is productively used in a company's

operations.

Plant assets are assets used in a company's operations that have a useful life of more than one

accounting period.

A delivery van that cost $45,000 with accumulated depreciation of $15,000 Is sold for $20,000. How

much gain or loss will be recognized on this sale?

$10,000 gain

$20,000 loss

$15,000 gain

$5,000 loss

$20,000 gain

$10,000 loss

Assume the company estimates that 5% of its accounts receivable will never be collected. a. Prepare the proper journal entry to recognize the expense

Assume the company estimates that 5% of its accounts receivable

will never be collected.

a. Prepare the proper journal entry to recognize the expense

involved.

Bad Debts Expense 2,000

Allowance for Doubtful Accounts 2,000

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

Accounts Receivable .................................................$800,000

Less: Allowance for Doubtful Accounts ........ 40,000

Estimated Realizable Accounts Receivable .$760,000

will never be collected.

a. Prepare the proper journal entry to recognize the expense

involved.

Bad Debts Expense 2,000

Allowance for Doubtful Accounts 2,000

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

Accounts Receivable .................................................$800,000

Less: Allowance for Doubtful Accounts ........ 40,000

Estimated Realizable Accounts Receivable .$760,000

Under assumptions 1 and 2 above, give the proper journal entries for

the following events.

June 3 John Shifty, who owes us $500, informs us that

he is broke and cannot pay. We believe him.

Nov. 9 We learned that John Shifty has won the lottery and

is willing to pay off all his old debts

.

June 3 Allowance for Doubtful Accounts............. 500

Accounts Receivable, John Shifty....... 500

Nov. 9 Accounts Receivable, John Shifty............ 500

Allowance for Doubtful Accounts........ 500

At the end of the year, the M. I. Wright Company showed the following selected account balances:

At the end of the year, the M. I. Wright Company showed the following

selected account balances:

Sales (all on credit) ............................................................................$300,000

Accounts Receivable ......................................................................... 800,000

Allowance for Doubtful Accounts..................................................... 38,000

Required:

1. Assume the company estimates that 1% of all credit sales will not be

collected.

a. Prepare the proper journal entry to recognize the expense

involved.

Bad Debts Expense 3,000

Allowance for Doubtful Accounts 3,000

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

Accounts Receivable .................................................$800,000

Less: Allowance for Doubtful Accounts ........ 41,000

Estimated Realizable Account Receivable….$759,000

selected account balances:

Sales (all on credit) ............................................................................$300,000

Accounts Receivable ......................................................................... 800,000

Allowance for Doubtful Accounts..................................................... 38,000

Required:

1. Assume the company estimates that 1% of all credit sales will not be

collected.

a. Prepare the proper journal entry to recognize the expense

involved.

Bad Debts Expense 3,000

Allowance for Doubtful Accounts 3,000

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

Accounts Receivable .................................................$800,000

Less: Allowance for Doubtful Accounts ........ 41,000

Estimated Realizable Account Receivable….$759,000

Mayfair Co. allows select customers to make purchases on credit. Its other customers can use either of two credit cards: Zisa or Access

Mayfair Co. allows select customers to make purchases on credit. Its other customers can use either of

two credit cards: Zisa or Access. Zisa deducts a 3% service charge for sales on its credit card and

credits the bank account of Mayfair immediately when credit card receipts are deposited. Mayfair

deposits the Zisa credit card receipts each business day. When customers use Access credit cards,

Mayfair accumulates the receipts for several days before submitting them to Access for payment.

Access deducts a 2% service charge and usually pays within one week of being billed. Mayfair

completes the following transactions in June. (The terms of all credit sales are 2/1 5, n/30, and all sales

are recorded at the gross price.)

June 4 Sold $650 of merchandise (that had cost $400) on credit to Natara Morris.

5 Sold $6,900 of merchandise (that had cost $4,200) to customers who used their Zisa cards.

6 Sold $5,850 of mercl1andise (that had cost $3,800) to customers who used their Access cards.

8 Sold $4.350 of merchandise (that had cost $2,900) to customers who used their Access cards.

10 Submitted Access card receipts accumulated since June 6 to the credit card company for

payment.

13 Wrote off the account of Abigail McKee against the Allowance for Doubtful Accounts. The $429

balance in McKee's account stemmed from a credit sale in October of last year.

17 Received the amount due from Access.

18 Received Morris's check in full payment for the purchase of June 4.

Required:

Prepare journal entries to record the preceding transactions and events. (The company uses the

perpetual inventory system.) (If no entry is required for a particular transaction, select "No journal

entry required" in the first account field.)

two credit cards: Zisa or Access. Zisa deducts a 3% service charge for sales on its credit card and

credits the bank account of Mayfair immediately when credit card receipts are deposited. Mayfair

deposits the Zisa credit card receipts each business day. When customers use Access credit cards,

Mayfair accumulates the receipts for several days before submitting them to Access for payment.

Access deducts a 2% service charge and usually pays within one week of being billed. Mayfair

completes the following transactions in June. (The terms of all credit sales are 2/1 5, n/30, and all sales

are recorded at the gross price.)

June 4 Sold $650 of merchandise (that had cost $400) on credit to Natara Morris.

5 Sold $6,900 of merchandise (that had cost $4,200) to customers who used their Zisa cards.

6 Sold $5,850 of mercl1andise (that had cost $3,800) to customers who used their Access cards.

8 Sold $4.350 of merchandise (that had cost $2,900) to customers who used their Access cards.

10 Submitted Access card receipts accumulated since June 6 to the credit card company for

payment.

13 Wrote off the account of Abigail McKee against the Allowance for Doubtful Accounts. The $429

balance in McKee's account stemmed from a credit sale in October of last year.

17 Received the amount due from Access.

18 Received Morris's check in full payment for the purchase of June 4.

Required:

Prepare journal entries to record the preceding transactions and events. (The company uses the

perpetual inventory system.) (If no entry is required for a particular transaction, select "No journal

entry required" in the first account field.)

Warner Company's year-end unadjusted trial balance shows accounts receivable of $99,000, allowance for doubtful accounts of $600

Warner Company's year-end unadjusted trial balance shows accounts receivable of $99,000,

allowance for doubtful accounts of $600 (credit), and sales of $280,000. Uncollectibles are estimated to

be 1.5% of accounts receivable.

1. Prepare the December 31 year-end adjusting entr1 for uncollectibles

2. What amount would have been used in the· year-end adjusting entry if the allowance account had a

year-end unadjusted debit balance of $300?

The following data are taken from the comparative balance sheets of Ruggers Company.

2013

Accounts receivable, net $153,400

Net sales 861,105

2012

$138,500

910,600

Complete the below table to calculate the accounts receivable turnover for the year 2013.

allowance for doubtful accounts of $600 (credit), and sales of $280,000. Uncollectibles are estimated to

be 1.5% of accounts receivable.

1. Prepare the December 31 year-end adjusting entr1 for uncollectibles

2. What amount would have been used in the· year-end adjusting entry if the allowance account had a

year-end unadjusted debit balance of $300?

The following data are taken from the comparative balance sheets of Ruggers Company.

2013

Accounts receivable, net $153,400

Net sales 861,105

2012

$138,500

910,600

Complete the below table to calculate the accounts receivable turnover for the year 2013.

Morales Company recorded the following selected transactions during November 2013.

Morales Company recorded the following selected transactions during November 2013.

Date General Journal Debit Credit

Nov. 5 Accounts Receivable- Ski Shop 4,670

Sales 4,670

10 Accounts Receivable- Welcome Enterprises 2,435

Sales 2,435

13 Accounts Receivable- Zia Natara 1,428

Sales 1,428

21 Sales Returns and Allowances 368

Accounts Receivable- Zia Natara 368

30 Accounts Receivable- Ski Shop 5,076

Sales 5,076

Prepare a general ledger having T-accounts for Accounts Receivable, Sales, and Sales Returns

and Allowances. Also open an accounts receivable subsidiary ledger having a T-account for each

customer. Post these entries to both the general ledger and the accounts receivable ledger.

2. Prepare a schedule of accounts receivable.

Date General Journal Debit Credit

Nov. 5 Accounts Receivable- Ski Shop 4,670

Sales 4,670

10 Accounts Receivable- Welcome Enterprises 2,435

Sales 2,435

13 Accounts Receivable- Zia Natara 1,428

Sales 1,428

21 Sales Returns and Allowances 368

Accounts Receivable- Zia Natara 368

30 Accounts Receivable- Ski Shop 5,076

Sales 5,076

Prepare a general ledger having T-accounts for Accounts Receivable, Sales, and Sales Returns

and Allowances. Also open an accounts receivable subsidiary ledger having a T-account for each

customer. Post these entries to both the general ledger and the accounts receivable ledger.

2. Prepare a schedule of accounts receivable.

Following are selected transactions for Ridge Company. Mar. 21 Accepted a $3,400, 180-0ay, 8% note dated March 21 from Tamara Jackson

Following are selected transactions for Ridge Company.

Mar. 21 Accepted a $3,400, 180-0ay, 8% note dated March 21 from Tamara Jackson in granting a time

extension on her past-due account receivable.

Sept 17 Jackson dishonors her note when it is presented for payment

Dec. 31 After exhausting all legal means of collection, Ridge Company writes off Jackson's account

against the Allowance for Doubtful Accounts.

First, complete the table below to calculate the interest amounts at September 17. (Use 360 days a

year.)

Use the calculated value to prepare your journal entries.

Mar. 21 Accepted a $3,400, 180-0ay, 8% note dated March 21 from Tamara Jackson in granting a time

extension on her past-due account receivable.

Sept 17 Jackson dishonors her note when it is presented for payment

Dec. 31 After exhausting all legal means of collection, Ridge Company writes off Jackson's account

against the Allowance for Doubtful Accounts.

First, complete the table below to calculate the interest amounts at September 17. (Use 360 days a

year.)

Use the calculated value to prepare your journal entries.

At year-end (December 31), Chan Company estimates its bad debts as 0.50% of its annual credit sales of $604,000. Chan records its Bad Debts Expense

At year-end (December 31), Chan Company estimates its bad debts as 0.50% of its annual credit sales

of $604,000. Chan records its Bad Debts Expense for that estimate. On the following February 1, Chan

decides that the $302 account of P. Park is uncollectible and writes it off as a bad debt. On June 5, Park

unexpectedly pays the amount previously written off.

Prepare the journal entries of Chan to record these transactions and events of December 31, February

1, and June 5.

On August 2, 2013, Jun Co. receives a $6,000, 90-0ay, 12% note from customer Ryan Albany as

payment on his $6,000 account.

Prepare the journal entry assuming the note is honored by the customer on October 31, 2013. (Use

360 days a year.)

of $604,000. Chan records its Bad Debts Expense for that estimate. On the following February 1, Chan

decides that the $302 account of P. Park is uncollectible and writes it off as a bad debt. On June 5, Park

unexpectedly pays the amount previously written off.

Prepare the journal entries of Chan to record these transactions and events of December 31, February

1, and June 5.

On August 2, 2013, Jun Co. receives a $6,000, 90-0ay, 12% note from customer Ryan Albany as

payment on his $6,000 account.

Prepare the journal entry assuming the note is honored by the customer on October 31, 2013. (Use

360 days a year.)

Liang Company began operations on January 1, 2012. During its first two years, the company completed a number of transactions involving sales on credit,

Liang Company began operations on January 1, 2012. During its first two years, the company

completed a number of transactions involving sales on credit, accounts receivable collections, and bad

debts. These transactions are summarized as follows:

2012

a. Sold $1,345,434 of merchandise (that had cost $975,000) on credit, terms n/30.

b. Wrote off$18,300 of uncollectible accounts receivable.

c. Received $669,200 cash in payment of accounts receivable.

d. In adjusting the accounts on December 31, the company estimated that 1.5% of accounts receivable

will be uncollectible.

2013

e. Sold $1,525,634 of merchandise (that had cost $1,250,000) on credit, terms n/30.

t. Wrote off $27,800 of uncollectible accounts receivable.

g. Received $1,204,600 cash in payment of accounts receivable.

h. In adjusting the accounts on December 31, the company estimated that 1.5% of accounts receivable

will be uncollectible.

Required:

Prepare journal entries to record Liang's 20 12 summarized transactions and its year-end adjustments

to record bad debts expense. (The company uses the perpetual inventor/ system and it applies the

allowance method for its accounts receivable.) (Round your intermediate calculations to the nearest

dollar amount.)

Prepare journal entries to record Liang's 20 13 summarized transactions and its year-end adjustments

to record bad debts expense. (The company uses the perpetual inventory system and it applies the

allowance method for its accounts receivable.) (Round your intermediate calculations to the nearest

dollar amount.)

completed a number of transactions involving sales on credit, accounts receivable collections, and bad

debts. These transactions are summarized as follows:

2012

a. Sold $1,345,434 of merchandise (that had cost $975,000) on credit, terms n/30.

b. Wrote off$18,300 of uncollectible accounts receivable.

c. Received $669,200 cash in payment of accounts receivable.

d. In adjusting the accounts on December 31, the company estimated that 1.5% of accounts receivable

will be uncollectible.

2013

e. Sold $1,525,634 of merchandise (that had cost $1,250,000) on credit, terms n/30.

t. Wrote off $27,800 of uncollectible accounts receivable.

g. Received $1,204,600 cash in payment of accounts receivable.

h. In adjusting the accounts on December 31, the company estimated that 1.5% of accounts receivable

will be uncollectible.

Required:

Prepare journal entries to record Liang's 20 12 summarized transactions and its year-end adjustments

to record bad debts expense. (The company uses the perpetual inventor/ system and it applies the

allowance method for its accounts receivable.) (Round your intermediate calculations to the nearest

dollar amount.)

Prepare journal entries to record Liang's 20 13 summarized transactions and its year-end adjustments

to record bad debts expense. (The company uses the perpetual inventory system and it applies the

allowance method for its accounts receivable.) (Round your intermediate calculations to the nearest

dollar amount.)

Gomez Corp. uses the allowance method to account for uncollectibles. On January 31, it wrote off a $800 account of a customer, C. Green

Gomez Corp. uses the allowance method to account for uncollectibles. On January 31, it wrote off a

$800 account of a customer, C. Green. On March 9, it receives a $300 payment from Green.

1. Prepare the journal entry for January 31.

2. Prepare the entries for March 9; assume no additional money is expected from Green.

Warner Company's year-end unadjusted trial balance shows accounts receivable of $99,000,

allowance for doubtful accounts of $600 (credit), and sales of $280,000. Uncollectibles are estimated to

be 0.5% of sales.

Prepare tl1e December 31 year-end adjusting entry for uncollectibles.

$800 account of a customer, C. Green. On March 9, it receives a $300 payment from Green.

1. Prepare the journal entry for January 31.

2. Prepare the entries for March 9; assume no additional money is expected from Green.

Warner Company's year-end unadjusted trial balance shows accounts receivable of $99,000,

allowance for doubtful accounts of $600 (credit), and sales of $280,000. Uncollectibles are estimated to

be 0.5% of sales.

Prepare tl1e December 31 year-end adjusting entry for uncollectibles.

Prepare journal entries for the following credit card sales transactions (the company uses the perpetual inventory system). 1. Sold $20,000 of merchandise, that cost $15,000, on MasterCard credit cards.

Prepare journal entries for the following credit card sales transactions (the company uses the perpetual

inventory system).

1. Sold $20,000 of merchandise, that cost $15,000, on MasterCard credit cards. The net cash receipts

from sales are immediately deposited in the seller's bank account. MasterCard charges a 5% fee.

2. Sold $5,000 of merchandise, that cost $3,000, on an assortment of credit cards. Net cash receipts

are received 5 days later, and a 4% fee is charged.

inventory system).

1. Sold $20,000 of merchandise, that cost $15,000, on MasterCard credit cards. The net cash receipts

from sales are immediately deposited in the seller's bank account. MasterCard charges a 5% fee.

2. Sold $5,000 of merchandise, that cost $3,000, on an assortment of credit cards. Net cash receipts

are received 5 days later, and a 4% fee is charged.

The following selected transactions are from Ohlmeyer Company. 2012 Dec. 16 Accepted a $10,800, 60-day, 8% note dated this day in granting Danny Todd

The following selected transactions are from Ohlmeyer Company.

2012

Dec. 16 Accepted a $10,800, 60-day, 8% note dated this day in granting Danny Todd a time extension

on his past-due account receivable.

31 Made an adjusting entry to record the accrued interest on the Todd note.

2013

Feb. 14 Received Todd's payment of principal and interest on the note dated December 16.

Mar. 2 Accepted an $6, 100, 8%, 90-day note dated this day in granting a time extension on the past·

due account receivable from Midnight Co.

17 Accepted a $2,400, 30-day, 7% note dated this day in granting Ava Privet a time extension on

her past-due account receivable.

Apr. 16 Privet dishonored her note when presented for payment.

June 2 Midnight Co. refuses to pay the note that was due to Ohlmeyer Co. on May 31. Prepare the

journal entry to c11arge the dishonored note plus accrued interest to Midnight Co.'s accounts

receivable.

July 17 Received payment from Midnight Co. for the maturity value of its dishonored note plus interest

for 46 days beyond maturity at 8%.

Aug. 7 Accepted an $7,450, 90-day, 10% note dated this day in granting a time extension on the

past-due account receivable of Mulan Co.

Sept. 3 Accepted a $2, 100, 60-day, 10% note dated this day in granting Noah Carson a time

extension on his past-due account receivable.

Nov. 2 Received payment of principal plus interest from Carson for the September 3 note.

Nov. 5 Received payment of principal plus interest from Mulan for the August 7 note.

Dec. 1 Wrote off the Privet account against Allowance for Doubtful Accounts.

(Do not round intermediate calculations . Use 360 days a year.)

Required:

First, complete the table below to calculate the interest amount at December 31.

2012

Dec. 16 Accepted a $10,800, 60-day, 8% note dated this day in granting Danny Todd a time extension

on his past-due account receivable.

31 Made an adjusting entry to record the accrued interest on the Todd note.

2013

Feb. 14 Received Todd's payment of principal and interest on the note dated December 16.

Mar. 2 Accepted an $6, 100, 8%, 90-day note dated this day in granting a time extension on the past·

due account receivable from Midnight Co.

17 Accepted a $2,400, 30-day, 7% note dated this day in granting Ava Privet a time extension on

her past-due account receivable.

Apr. 16 Privet dishonored her note when presented for payment.

June 2 Midnight Co. refuses to pay the note that was due to Ohlmeyer Co. on May 31. Prepare the

journal entry to c11arge the dishonored note plus accrued interest to Midnight Co.'s accounts

receivable.

July 17 Received payment from Midnight Co. for the maturity value of its dishonored note plus interest

for 46 days beyond maturity at 8%.

Aug. 7 Accepted an $7,450, 90-day, 10% note dated this day in granting a time extension on the

past-due account receivable of Mulan Co.

Sept. 3 Accepted a $2, 100, 60-day, 10% note dated this day in granting Noah Carson a time

extension on his past-due account receivable.

Nov. 2 Received payment of principal plus interest from Carson for the September 3 note.

Nov. 5 Received payment of principal plus interest from Mulan for the August 7 note.

Dec. 1 Wrote off the Privet account against Allowance for Doubtful Accounts.

(Do not round intermediate calculations . Use 360 days a year.)

Required:

First, complete the table below to calculate the interest amount at December 31.

Levine Company uses the perpetual inventory system and allows customers to use two credit cards in charging purchases. With the Suntrust Bank Card,

Levine Company uses the perpetual inventory system and allows customers to use two credit cards in

charging purchases. With the Suntrust Bank Card, Levine receives an immediate credit to its account

when it deposits sales receipts. Suntrust assesses a 4% service charge for credit card sales. The

second credit card that Levine accepts is the Continental Card. Levine sends its accumulated receipts

to Continental on a weekly basis and is paid by Continental about a week later. Continental assesses a

2.5% charge on sales for using its card.

Apr. 8 Sold merchandise for $7,800 (that had cost $5,764) and accepted the customer's Suntrust Bank

Card. The Suntrust receipts are immediately deposited in Levine's bank account.

12 Sold merchandise for $9,1 00 (that had cost $5,897) and accepted the customer's Continental

Card. Transferred $9,1 00 of credit card receipts to Continental, requesting payment.

20 Received Continental's check for the April 12 billing, less the service charge.

Prepare journal entries to record the above selected credit card transactions of Levine Company.

charging purchases. With the Suntrust Bank Card, Levine receives an immediate credit to its account

when it deposits sales receipts. Suntrust assesses a 4% service charge for credit card sales. The

second credit card that Levine accepts is the Continental Card. Levine sends its accumulated receipts

to Continental on a weekly basis and is paid by Continental about a week later. Continental assesses a

2.5% charge on sales for using its card.

Apr. 8 Sold merchandise for $7,800 (that had cost $5,764) and accepted the customer's Suntrust Bank

Card. The Suntrust receipts are immediately deposited in Levine's bank account.

12 Sold merchandise for $9,1 00 (that had cost $5,897) and accepted the customer's Continental

Card. Transferred $9,1 00 of credit card receipts to Continental, requesting payment.

20 Received Continental's check for the April 12 billing, less the service charge.

Prepare journal entries to record the above selected credit card transactions of Levine Company.

Conroy Company uses the allowance method to account for bad debts. During 2010, Conroy determined that a balance of $200 for Alegia Co

All of the following are similarities in valuing receivables using U.S. GAAP and IFRS except

expense for estimated uncollectibles must be recorded in the same period as the related

revenues

IFRS does not require the allowance method for uncollectibles

IFRS does Teguire the allowance method

receivables must be reported net of estimated uncollectibles

Conroy Company uses the allowance method to account for bad debts. During 2010, Conroy determined

that a balance of $200 for Alegia Co. was uncollectible and wrote the balance off. What is the total

decrease to net income related to this entry?

Cannot be Determined

$0

$200

When a note's maker is unable or refuses to pay at maturity, the note is considered dishonored.

The allowance for doubtful accounts is a(n) (current;contra/opposite)contra asset account and has a

normal credit balance.

expense for estimated uncollectibles must be recorded in the same period as the related

revenues

IFRS does not require the allowance method for uncollectibles

IFRS does Teguire the allowance method

receivables must be reported net of estimated uncollectibles

Conroy Company uses the allowance method to account for bad debts. During 2010, Conroy determined

that a balance of $200 for Alegia Co. was uncollectible and wrote the balance off. What is the total

decrease to net income related to this entry?

Cannot be Determined

$0

$200

When a note's maker is unable or refuses to pay at maturity, the note is considered dishonored.

The allowance for doubtful accounts is a(n) (current;contra/opposite)contra asset account and has a

normal credit balance.

Lani Co. uses the allowance method to account for bad debts. At the end of 2010, their unadjusted trial balance shows an accounts receivable balance of $400,000

Lani Co. uses the allowance method to account for bad debts. At the end of 2010, their unadjusted trial

balance shows an accounts receivable balance of $400,000; allowance for doubtful accounts balance of

$400 (debit); and sales of $1,200,000. Based on history, Lani estimates that bad debts will be 1% of

accounts receivable. The entry to record estimated bad debts will include a debit to Bad Debts Expense in

the amount of:

$3,600

$12,400

$4.400

$11,600

$12,000

$4,000

The realization principle under IFRS refers to the following:

risk transfer and ownership reward

an arm's length transaction and economic benefits

reliable measurement and likelihood of economic benefits

Avi Co. raises cash by borrowing $10,000 and pledging $12,000 accounts receivables as security for the

loan. To comply with the full disclosure principle, Avi will record a journal entry in the amount of the

$10,000 note payable, and also record a (debit/credit/note)note to the financial statements, indicating

that $12,000 of accounts receivables have been pledged.

At year-end, Yates Company estimates that $1,500 of its accounts receivable balance is uncollectible.

Yates uses the allowance method to account for bad debts. The entry to record this adjusting entry would

include a:

debit to Allowance for Doubtful Accounts and credit to Bad Debts Expense

debit to Bad Debts Expense and credit to Accounts Receivable

debit to Bad Debts Expense and credit to Allowance for Doubtful Accounts

debit to Accounts Receivable and credit to Bad Debts Expense

balance shows an accounts receivable balance of $400,000; allowance for doubtful accounts balance of

$400 (debit); and sales of $1,200,000. Based on history, Lani estimates that bad debts will be 1% of

accounts receivable. The entry to record estimated bad debts will include a debit to Bad Debts Expense in

the amount of:

$3,600

$12,400

$4.400

$11,600

$12,000

$4,000

The realization principle under IFRS refers to the following:

risk transfer and ownership reward

an arm's length transaction and economic benefits

reliable measurement and likelihood of economic benefits

Avi Co. raises cash by borrowing $10,000 and pledging $12,000 accounts receivables as security for the

loan. To comply with the full disclosure principle, Avi will record a journal entry in the amount of the

$10,000 note payable, and also record a (debit/credit/note)note to the financial statements, indicating

that $12,000 of accounts receivables have been pledged.

At year-end, Yates Company estimates that $1,500 of its accounts receivable balance is uncollectible.

Yates uses the allowance method to account for bad debts. The entry to record this adjusting entry would

include a:

debit to Allowance for Doubtful Accounts and credit to Bad Debts Expense

debit to Bad Debts Expense and credit to Accounts Receivable

debit to Bad Debts Expense and credit to Allowance for Doubtful Accounts

debit to Accounts Receivable and credit to Bad Debts Expense

Flash Co. uses the allowance method to account for bad debts. At the end of 2010, Flash Co.'s unadjusted trial balance

Flash Co. uses the allowance method to account for bad debts. At the end of 2010, Flash Co.'s

unadjusted trial balance shows an accounts receivable balance of $45,000; allowance for doubtful

accounts balance of $400 (debit); and sales of $1,500,000. Based on history, Flash estimates that bad

debts will be 0.5% of sales. The entry to record estimated bad debts will include an debit to Bad Debts

Expense ln the amount of:

$7,100

$7,500

$795,000

$750,000

$7,900

The ____ method of estimating bad debts uses both past and current receivables information to

estimate the allowance amount. Specifically, each receivable is classified by how long it is past its due

date.

percentage of sales

aging of receivable

percentage of receivables

The following financial information is available for Si u Co.

2010 2009

Net Sales 160,000 155,000

Accounts Receivable 38,000 32,000

Compute accounts receivable turnover for 2010. Round your answer to one decimal place.

4.5

4.6

4.8

4.2

unadjusted trial balance shows an accounts receivable balance of $45,000; allowance for doubtful

accounts balance of $400 (debit); and sales of $1,500,000. Based on history, Flash estimates that bad

debts will be 0.5% of sales. The entry to record estimated bad debts will include an debit to Bad Debts

Expense ln the amount of:

$7,100

$7,500

$795,000

$750,000

$7,900

The ____ method of estimating bad debts uses both past and current receivables information to

estimate the allowance amount. Specifically, each receivable is classified by how long it is past its due

date.

percentage of sales

aging of receivable

percentage of receivables

The following financial information is available for Si u Co.

2010 2009

Net Sales 160,000 155,000

Accounts Receivable 38,000 32,000

Compute accounts receivable turnover for 2010. Round your answer to one decimal place.

4.5

4.6

4.8

4.2

Tricon Co. sells $10,000 of Its accounts receivables and is charged a 5% factoring fee. It records this sale with a debit to:

The ____ method, also referred to as balance sheet method, uses balance sheet relations to

estimate bad debts-mainly, the relationship between accounts receivable and the allowance account.

accounts receivable

allowance

bad debts

percentage of sales

Tricon Co. sells $10,000 of Its accounts receivables and is charged a 5% factoring fee. It records this sale

with a debit to:

Accounts Receivable for $10,000.

Cash for $10,000.

Cash for $10,500.

Cash for $9,500.

Accounts Receivable for $10,500.

Accounts Receivable for $9,500.

Companies sometimes convert receivables to cash before they are due by selling them or using them as

security for a loan. The reasons that a company may convert receivables before their due date include:

(Check all that apply.)

to satisfy customer's needs.

to quickly increase profit.

to reduce risk of nonpayment.

to quickly generate cash.

Although U.S. GMP and IFRS have similar rules in recording disposition of receivables, Under U.S. GMP

provision refers to expense. Under IFRS, provision refers to

An asset

A liability

A revenue

estimate bad debts-mainly, the relationship between accounts receivable and the allowance account.

accounts receivable

allowance

bad debts

percentage of sales

Tricon Co. sells $10,000 of Its accounts receivables and is charged a 5% factoring fee. It records this sale

with a debit to:

Accounts Receivable for $10,000.

Cash for $10,000.

Cash for $10,500.

Cash for $9,500.

Accounts Receivable for $10,500.

Accounts Receivable for $9,500.

Companies sometimes convert receivables to cash before they are due by selling them or using them as

security for a loan. The reasons that a company may convert receivables before their due date include:

(Check all that apply.)

to satisfy customer's needs.

to quickly increase profit.

to reduce risk of nonpayment.

to quickly generate cash.

Although U.S. GMP and IFRS have similar rules in recording disposition of receivables, Under U.S. GMP

provision refers to expense. Under IFRS, provision refers to

An asset

A liability

A revenue

Acel Co. uses the allowance method to account for bad debts. Early In 2010, Ace I determined that It could not collect $400 from CTR

Acel Co. uses the allowance method to account for bad debts. Early In 2010, Ace I determined that It

could not collect $400 from CTR, Inc. and wrote the balance off. On October 21, Acel received a check for

$400 from CTR. The entries to record the receipt of cash on October 21 would include a debit to:

Select two answers .

could not collect $400 from CTR, Inc. and wrote the balance off. On October 21, Acel received a check for

$400 from CTR. The entries to record the receipt of cash on October 21 would include a debit to:

Select two answers .

Accounts Receivable.

Accounts receivable is debited to reinstate

Allowance for Doubtful Accounts.

Bad Debt Expense.

cash.

Zlno Company determines that a customer balance of $200,from Hollis Co. is uncollectible. Zino uses the

allowance method to account for bad debts. The entry to write off the uncollectible balance will include a:

debit to Allowance for Doubtful Accounts and a credit to Accounts Receivable.

debit to Bad Debts Expense and a credit to Allowance for Doubtful Accounts.

debit to Accounts Receivable and a credit to Allowance for Doubtful Accounts.

debit to Allowance for Doubtful Accounts and a credit to Bad Debts Expense.

The expected proceeds from accounts receivable, determined by taking accounts receivable less the

allowance for doubtful accounts, is called:

contra receivables

accounts receivable turnover

total receivables

realizable value

The principal and interest of a note are due on its maturity date. The maker of the note usually

(makes/honors/dishonors)honors the note and pays it in full.

Companies sometimes convert receivables to cash before they are due. When a company sells its

receivables, it is called factoring (pledging/factoring). When a company uses receivables as collateral for

a bank loan, it is called pledging (pledging/factoring).

On November 1, Alice Co. accepted a 9Q..day, 6%, 2,000 note due January 30. On 12/31, the appropriate adjusting entry was made on 12/31

On November 1, Alice Co. accepted a 9Q..day, 6%, 2,000 note due January 30. On 12/31, the appropriate adjusting entry was made on 12/31. On January 30, the note was honored and paid in full. The entry to record receipt of payment on January 30 would include a credit to: (Check all that apply.)

Interest Receivable for $20.

Cash for $2,030.

Notes Receivable for $2,000

Interest Revenue for $30.

Interest Revenue for $20.

Interest Revenue for $10.

DonCo, Inc. sold merchandise on January 14, and accepted a 90-day, 5% promissory note in the amount

of $5,000. On January 14, the entry to record this transaction would include a debit to:

Notes Receivable In the amount of $5,000

Sales in the amount of $5,000

Accounts Receivable In the amount of $5,000

Cash in the amount of $5,000

Kaiven Company accepted a $12,000, 60-day, 6% note on December 21 from Diaz Co, granting a time

extension on his past-due account receivable. The adjusting entry on December 31 would include a debit

to:

Interest Receivable for $120.

Interest Receivable for $20.

Interest Revenue for $120.

Interest Revenue for $20.

Interest Receivable for $20.

Cash for $2,030.

Notes Receivable for $2,000

Interest Revenue for $30.

Interest Revenue for $20.

Interest Revenue for $10.

DonCo, Inc. sold merchandise on January 14, and accepted a 90-day, 5% promissory note in the amount

of $5,000. On January 14, the entry to record this transaction would include a debit to:

Notes Receivable In the amount of $5,000

Sales in the amount of $5,000

Accounts Receivable In the amount of $5,000

Cash in the amount of $5,000

Kaiven Company accepted a $12,000, 60-day, 6% note on December 21 from Diaz Co, granting a time

extension on his past-due account receivable. The adjusting entry on December 31 would include a debit

to:

Interest Receivable for $120.

Interest Receivable for $20.

Interest Revenue for $120.

Interest Revenue for $20.

On January 1, Franz Co. accepted a 3o-day, 6% note in the amount of $5,000 from Bria Co., a customer. On January 31, the due date of the note

JD Co. had $1,000 of credit cards sales. The net cash receipts were deposited Immediately Into

Whitlock's bank account less a 3% fee. The entry to record this sales transaction would include the

following debit entries. (Check all that apply.)

Sales for $970

Cash for $970

Accounts Receivable for $970

Accounts Receivable for $1,000

Credit card Expense for $30

cash for $1,000

The _____ method of accounting for bad debts records the loss from an uncollectible account

receivable when it is determined to be uncollectible. No attempt is made to predict bad debts expense.

percentage of sales

direct write-off

allowance

percentage of receivables

On January 1, Franz Co. accepted a 3o-day, 6% note in the amount of $5,000 from Bria Co., a customer.

On January 31, the due date of the note, Bria honors the note and pays In full. The journal entry that

Franz would make to record payment of this note would include a: (Check all that apply.)

debit to Cash for $5,025.

credit to Note Receivable for $5,025.

credit to Note Receivable for $5,000.

debit to Interest Revenue for $25.

credit to Interest Revenue for $25.

Whitlock's bank account less a 3% fee. The entry to record this sales transaction would include the

following debit entries. (Check all that apply.)

Sales for $970

Cash for $970

Accounts Receivable for $970

Accounts Receivable for $1,000

Credit card Expense for $30

cash for $1,000

The _____ method of accounting for bad debts records the loss from an uncollectible account

receivable when it is determined to be uncollectible. No attempt is made to predict bad debts expense.

percentage of sales

direct write-off

allowance

percentage of receivables

On January 1, Franz Co. accepted a 3o-day, 6% note in the amount of $5,000 from Bria Co., a customer.

On January 31, the due date of the note, Bria honors the note and pays In full. The journal entry that

Franz would make to record payment of this note would include a: (Check all that apply.)

debit to Cash for $5,025.

credit to Note Receivable for $5,025.

credit to Note Receivable for $5,000.

debit to Interest Revenue for $25.

credit to Interest Revenue for $25.

Tuesday, November 26, 2019

On March 14, Ian Co. accepted a 180-day, 5% note in the amount of $1,000 from Ali Co., a customer. On the due date of the note

On March 14, Ian Co. accepted a 180-day, 5% note in the amount of $1,000 from Ali Co., a customer. On

the due date of the note, Ali dishonors the note and fails to pay. The journal entry that Ian would record

on the due date would include a: (Check all that apply.)

debit to Accounts Receivable -All for $1,025.

$1,000 x (180/360) x .05 = $25 interest

debit to Interest Revenue for $25.

credit to Notes Receivable for $1,000.

credit to Accounts Receivable -Ali for $1,000.

debit to Notes Receivable for $1,025.

credit to Interest Revenue for $25.

1,000 x (1.80/360) x .05= $25 interest

On February 15, Symth Co. determines that It cannot collect $500 owed by Its customer, A. Winds. Symth

records the loss using the direct write-off method. This entry to record the write-off on February 15 would

Include a: (Check all that apply.)

credit to Bad Debts Expense.

credit to Sales.

debit to Sales.

debit to Accounts Receivable - A. Winds.

debit to Bad Debts Expense.

credit to Accounts Receivable - A. Winds.

Simon Co. sold $500 of merchandise on credit cards. The net cash receipts are received 10 days later,

less a 2% fee. The entry to record this sales transaction on the date of the sale would Include a debit to:

cash for $490

Sales for $490

cash for $500

Sales for $500

Accounts Receivable for $500

Accounts Receivable for $490

the due date of the note, Ali dishonors the note and fails to pay. The journal entry that Ian would record

on the due date would include a: (Check all that apply.)

debit to Accounts Receivable -All for $1,025.

$1,000 x (180/360) x .05 = $25 interest

debit to Interest Revenue for $25.

credit to Notes Receivable for $1,000.

credit to Accounts Receivable -Ali for $1,000.

debit to Notes Receivable for $1,025.

credit to Interest Revenue for $25.

1,000 x (1.80/360) x .05= $25 interest

On February 15, Symth Co. determines that It cannot collect $500 owed by Its customer, A. Winds. Symth

records the loss using the direct write-off method. This entry to record the write-off on February 15 would

Include a: (Check all that apply.)

credit to Bad Debts Expense.

credit to Sales.

debit to Sales.

debit to Accounts Receivable - A. Winds.

debit to Bad Debts Expense.

credit to Accounts Receivable - A. Winds.

Simon Co. sold $500 of merchandise on credit cards. The net cash receipts are received 10 days later,

less a 2% fee. The entry to record this sales transaction on the date of the sale would Include a debit to:

cash for $490

Sales for $490

cash for $500

Sales for $500

Accounts Receivable for $500

Accounts Receivable for $490

A. Stine Co. previously wrote off a $200 bad debt from Thorn Co. using the direct write-off method. On October 1, Stine unexpectedly receives a check

In July, Lane Co. sells merchandise to Avery Co. on account. In August, Avery pays the balance in full. The

entry that Lane will make to record the receipt of cash will include a credit to the account.

Accounts Payable

Sales

Accounts Receivable

Cash

Unearned Sales

To compute interest due on a maturity date, you should multiply which of the following factors? (Check all

that apply.)

Time expressed in fraction of year

Maturity value

Principal

Interest Rate

On June 30, Nance Company receives a $5,000, 90-day, 4% note from a customer as payment on her

account How much interest will be due on the note's maturity date?

$225

$50

$200

$25

A 90-day note is signed on October 21. The due date of the note is:

January 21

January 20

January 18

January 19

A. Stine Co. previously wrote off a $200 bad debt from Thorn Co. using the direct write-off method. On

October 1, Stine unexpectedly receives a check in the amount of $200 from Thom Co. The entry to record

this receipt of $200 will include a: (Check all that apply.)

credit to cash.

debit to cash.

credit to Bad Debts Expense

debit to Bad Debts Expense

entry that Lane will make to record the receipt of cash will include a credit to the account.

Accounts Payable

Sales

Accounts Receivable

Cash

Unearned Sales

To compute interest due on a maturity date, you should multiply which of the following factors? (Check all

that apply.)

Time expressed in fraction of year

Maturity value

Principal

Interest Rate

On June 30, Nance Company receives a $5,000, 90-day, 4% note from a customer as payment on her

account How much interest will be due on the note's maturity date?

$225

$50

$200

$25

A 90-day note is signed on October 21. The due date of the note is:

January 21

January 20

January 18

January 19

A. Stine Co. previously wrote off a $200 bad debt from Thorn Co. using the direct write-off method. On

October 1, Stine unexpectedly receives a check in the amount of $200 from Thom Co. The entry to record

this receipt of $200 will include a: (Check all that apply.)

credit to cash.

debit to cash.

credit to Bad Debts Expense

debit to Bad Debts Expense

The following information is available for Johnson Manufacturing Company at June 30:

1. The following information is available for Holland Company at December 31:

Based on this information, Holland Company should report Cash and Cash Equivalents on December 31 of:

$35,421

2. The following information is available for Johnson Manufacturing Company at June 30:

Based on this information, Johnson Manufacturing Company should report Cash and Cash Equivalents on June 30 of:

$19,462

3. At the end of the current period, a company reported $475,000 in net credit sales and $75,000 in ending

accounts receivable. Calculate this company's days' sales uncollected at the end of the current period.

57.63 days

4. On August 17, at the end of the day, the cash register's record shows $957, but the count of cash in the

register is $965. Prepare the general journal entry to record the day's cash sales.

Based on this information, Holland Company should report Cash and Cash Equivalents on December 31 of:

$35,421

2. The following information is available for Johnson Manufacturing Company at June 30:

Based on this information, Johnson Manufacturing Company should report Cash and Cash Equivalents on June 30 of:

$19,462

3. At the end of the current period, a company reported $475,000 in net credit sales and $75,000 in ending

accounts receivable. Calculate this company's days' sales uncollected at the end of the current period.

57.63 days

4. On August 17, at the end of the day, the cash register's record shows $957, but the count of cash in the

register is $965. Prepare the general journal entry to record the day's cash sales.

Following are seven items a through g that would cause Xavier Company's book balance of cash ($2,451)to differ from its bank statement balance of cash. ($2,000)

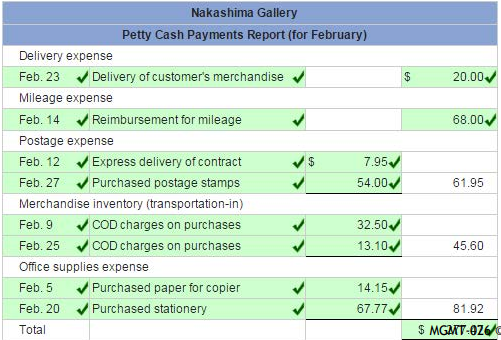

A company established a petty cash fund of $100 on September 1. On September 10, the petty cash fund was

replenished when there was $16 remaining and there were petty cash receipts for: office supplies, $27;

transportation-in on inventory purchased, $32; and postage, $22. On September 15, the petty cash fund was

increased to $125 in total. Record the above transactions in general journal form.

Following are seven items a through g that would cause Xavier Company's book balance of cash ($2,451)to

differ from its bank statement balance of cash. ($2,000)

a. A service charge imposed by the bank.$20

b. A check listed as outstanding on the previous period's reconciliation and still outstanding at the end of this

month.$100

c. A customer's check returned by the bank is marked "Not Sufficient Funds(NSF)".$200

d. A deposit that was mailed to the bank on the last day of the current month and is unrecorded on this month's

bank statement.$700

e. A check paid by the bank at its correct $190 amount was recorded in error in the company's Check Register at

$109.

f. An unrecorded credit memorandum indicated that bank had collected a note receivable for Xavier Company

and deposited the proceeds in the company's account.$300

g. A check was written in the current period that is not yet paid or returned by the bank.$150

Indicate where each item a through g would appear on Xavier Company's bank reconciliation by placing its

identifying letter in the parentheses in the proper section of the form below.

replenished when there was $16 remaining and there were petty cash receipts for: office supplies, $27;

transportation-in on inventory purchased, $32; and postage, $22. On September 15, the petty cash fund was

increased to $125 in total. Record the above transactions in general journal form.

Following are seven items a through g that would cause Xavier Company's book balance of cash ($2,451)to

differ from its bank statement balance of cash. ($2,000)

a. A service charge imposed by the bank.$20

b. A check listed as outstanding on the previous period's reconciliation and still outstanding at the end of this

month.$100

c. A customer's check returned by the bank is marked "Not Sufficient Funds(NSF)".$200

d. A deposit that was mailed to the bank on the last day of the current month and is unrecorded on this month's

bank statement.$700

e. A check paid by the bank at its correct $190 amount was recorded in error in the company's Check Register at

$109.

f. An unrecorded credit memorandum indicated that bank had collected a note receivable for Xavier Company

and deposited the proceeds in the company's account.$300

g. A check was written in the current period that is not yet paid or returned by the bank.$150

Indicate where each item a through g would appear on Xavier Company's bank reconciliation by placing its

identifying letter in the parentheses in the proper section of the form below.

The Betsy Dough Company wants to prepare a bank reconciliation for the month of June. When the bank statement for the month of June arrives from the bank

The Betsy Dough Company wants to prepare a bank reconciliation for the

month of June. When the bank statement for the month of June arrives

from the bank, the following steps are performed:

1. The deposits to the bank account, as recorded on the bank statement,

are compared to the deposit slips retained by the company. It is noted

that the last deposit, of $400, occurred after banking hours on the day of

the bank statement and therefore has not been recorded by the bank on

this bank statement.

2. Checks returned with the bank statement are compared to the checks

written and listed in checkbook. This comparison shows that there are

checks outstanding amounting to $1,456.

3. The ending balances on the statement and in the company’s books are

determined. The ending bank statement balance is exactly $10,129

whereas the books show $9,000.

4. Other information contained on the bank statement, not previously

known to the company, is determined. This includes the following: (a) a

note from a customer for $200 has been collected by the bank and

credited to our account; (b) a check from Frank Ony for $120 previously

deposited by us has been returned for lack of sufficient funds; (c) the

bank has charged us $25 for its services (this includes a $10 fee for the

NSF check).

5. A bank reconciliation is prepared; it does not balance! The difference is

$18, so a transposition error is looked for (whenever the difference is a

multiple of 9, there is a very good chance that there has been an

inadvertent exchange of two digits (for example, writing 29 when it

should have been 92). An error is found. Check number 141 was written

for $235 and cleared the bank for $235, but was recorded in the

company records as $253.

Required:

1)Prepare a bank reconciliation for the Betsy Dough Company at June 30,

2011.

2)Prepare the appropriate journal entries.

month of June. When the bank statement for the month of June arrives

from the bank, the following steps are performed:

1. The deposits to the bank account, as recorded on the bank statement,

are compared to the deposit slips retained by the company. It is noted

that the last deposit, of $400, occurred after banking hours on the day of

the bank statement and therefore has not been recorded by the bank on

this bank statement.

2. Checks returned with the bank statement are compared to the checks

written and listed in checkbook. This comparison shows that there are

checks outstanding amounting to $1,456.

3. The ending balances on the statement and in the company’s books are

determined. The ending bank statement balance is exactly $10,129

whereas the books show $9,000.

4. Other information contained on the bank statement, not previously

known to the company, is determined. This includes the following: (a) a

note from a customer for $200 has been collected by the bank and